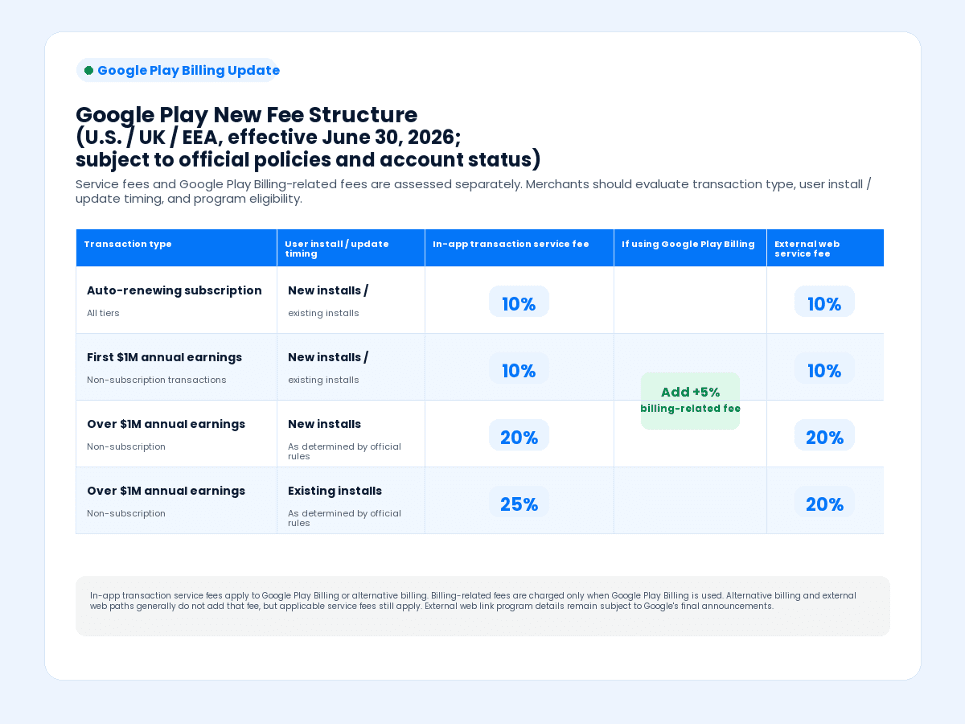

On June 30, 2026, Google Play began applying a new fee structure in the United States, the United Kingdom, and the European Economic Area (EEA). The public framework now separates Google Play service fees from Google Play Billing-related fees.

Whether a merchant uses Google Play Billing, alternative billing, or an external web purchase path, the applicable Google Play service fee still needs to be included in the calculation. If the merchant continues to use Google Play Billing, an additional billing-related fee of approximately 5% also applies under the public policy framework.

Public fee treatment is generally determined by whether the user first installs or updates the app after the effective date of the new fee structure in the relevant market. The final determination should be based on Google Play Console and Google’s official rules. For games or content businesses with a large installed base, non-recurring transactions from existing installs need to be evaluated by path: in-app transactions or alternative billing may be subject to a 25% service fee, while external web link transactions may be subject to a 20% service fee. At scale, that difference matters.

Part 1 of this series compared Apple and Google’s rules across the United States, the European Union, Japan, and South Korea, and introduced three external purchase paths. This article turns to operating outcomes: when part of the transaction flow moves away from platform-controlled billing, what should digital goods and services merchants actually calculate?

1. The fee difference is only the starting point

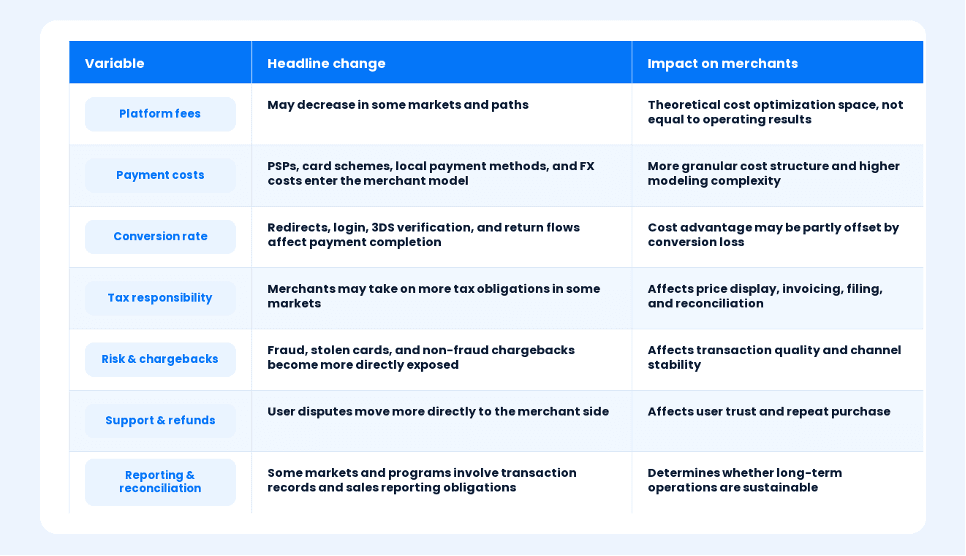

Platform service fees are often the most visible variable in the external purchase discussion. Traditional in-app purchase models can carry standard fees of up to 30%, which is material for game purchases, virtual items, short-drama unlocks, subscriptions, memberships, and paid content.

But once transactions move partially outside the platform billing flow, merchants also take on payment processing costs, tax calculation, dispute and chargeback handling, billing explanations, entitlement delivery, refund support, and financial reconciliation.

Take Google Play’s new fee structure as an example. In the United States, the United Kingdom, and the EEA, a subscription product for a short-drama or utility app may see its headline fee rate come in about 5 percentage points lower when using an external purchase path instead of continuing with Google Play Billing. The reason is straightforward: the service fee remains part of the calculation, while the additional Google Play Billing-related fee does not apply if Google Play Billing is not used.

That difference does not automatically translate into commercial upside. Payment service provider fees, tax operations, chargebacks, fraud losses, and redirect-related conversion loss can all vary significantly by product type and user segment.

Higher-ticket monthly subscriptions, stable renewals, and products such as game battle passes may be better candidates for early modeling. Low-price single-episode unlocks or small virtual-item purchases require a more careful review of payment friction.

In other words, 30%—or a lower applicable platform fee—should be treated as a headline reference point, not the final answer. The real question is the total cost of the full transaction path.

This is not a payment-team-only discussion. Product teams care about entry points and conversion. Finance teams care about tax and reconciliation. Legal teams care about platform rules and market restrictions. Operations and customer support teams care about refunds, complaints, and user trust. Target market, user segment, product type, and actual conversion performance all need to be part of the early calculation.

2. Conversion loss needs to be tested, not assumed

External purchase paths change the user journey. A user may move from the app to a web checkout, choose between different payment options, complete payment, and return to the app for entitlement confirmation. Friction at any point can affect transaction success.

That does not mean external purchase and billing options are unsuitable by default. For higher-value users, repeat buyers, and users with stronger brand trust, a well-designed path can still be worth testing. Several practical principles matter.

Entry point. Place the entry where purchase intent is already clear, such as a game top-up page, bundle detail page, short-drama unlock prompt, or membership renewal page.

User segmentation. High-spending players, monthly-card members, and long-term subscribers are often more tolerant of an extra step. For casual players or first-time payers, keeping familiar options such as IAP or Play Billing can reduce uncertainty.

Incentive design. Web-exclusive bundles, top-up bonuses, or membership discounts should be clear and specific. The messaging should not frame the platform billing option as the “wrong” choice. This is more aligned with platform rule expectations and helps preserve user trust.

Payment methods. Payment preferences vary by market. Showing familiar cards, local wallets, and other locally trusted methods can help reduce friction.

Return experience. After payment, entitlements should be activated quickly, billing descriptors should be recognizable, and refund routes should be clear.

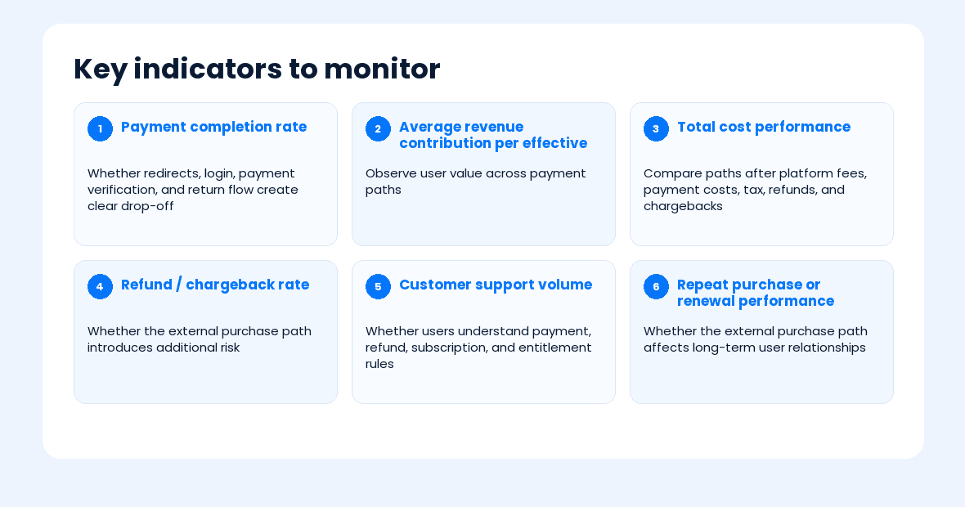

From a pilot-management perspective, merchants should usually start with a limited market, user segment, and product scope, then observe path performance before scaling. Key indicators include:

3. Operating responsibility determines whether the path can scale

Digital goods have distinct payment-risk characteristics. Game top-ups, virtual items, short-drama unlocks, subscriptions, and memberships are often delivered instantly, have low marginal cost, and can be copied or arbitraged. Once coins are credited or episodes are unlocked, disputes are harder to resolve by simply “taking back the product.”

When transactions move to a merchant-owned path, fraud, stolen-card use, refund disputes, and non-fraud chargebacks become more direct inputs into the merchant’s operating model.

Customer support pressure also increases. From the user’s point of view, a payment-path change becomes a series of specific entitlement questions: Did my game currency arrive? Why is this episode still locked? How do I cancel my subscription? Who handles my refund?

If these questions are not handled clearly, routine support tickets can escalate into complaints or negative reviews. For subscription and high-frequency purchase businesses, disputes affect more than one transaction. They can erode lifetime value.

Risk and support should therefore be built into the full transaction lifecycle, not handled only after a failed payment.

Before the transaction: monitor abnormal traffic and suspicious payment behavior to prevent stolen-card activity, bonus abuse, and other risks from accumulating before payment.

During the transaction: make prices, tax, subscription terms, promotion rules, and billing information clear.

After the transaction: provide clear refund, support, and dispute-handling processes. For subscription products, make cancellation routes explicit so users do not initiate chargebacks simply because they cannot find where to cancel.

Tax and finance also need to be planned within the same flow. When a merchant uses Apple IAP or Google Play Billing, indirect tax calculation, collection, and remittance may be handled by the platform in some markets. When the merchant switches to an external purchase flow or alternative billing, it may need to deal more directly with seller-of-record status, tax-inclusive pricing, tax calculation, invoices or receipts, refund reversals, and tax-data retention.

Tax responsibility, filing thresholds, and price-display rules vary significantly by market. U.S., EU, Japanese, and Korean tax rates were covered in Part 1 of this series. Registration, filing, withholding or remittance arrangements, and platform collection treatment still need to be confirmed based on the merchant entity, user location, product type, and transaction path. This article highlights tax as an operating variable and does not constitute tax advice.

For most merchants, external purchase and billing options do not require a full migration on day one. A more practical approach is to start with a market where the rules are relatively clear and the transaction base is stable, then use a suitable user and product sample to validate cost, experience, and operating boundaries before expanding.

For example, U.S. iOS external purchase link restrictions have been meaningfully relaxed. For game and subscription businesses with an established U.S. user base and meaningful revenue, the U.S. can be a useful early pilot market.

Once external purchase and billing options enter the evaluation and implementation stage, the questions usually spread across product, engineering, finance, legal, and operations teams. The core challenge for merchants is not “adding one more checkout.” It is reducing the decision cost of assessing, piloting, and scaling a new transaction path.

PayerMax can help merchants evaluate which markets, product types, and user paths are suitable for a pilot, while reducing implementation complexity across payment integration, risk and chargeback handling, tax and financial reconciliation, and operational record-keeping.

If you are evaluating whether external purchase and billing options fit your business, contact the PayerMax team to discuss target markets, product scenarios, user paths, and operating requirements.