Key takeaways

A new rule environment is taking shape. Court rulings, antitrust legislation, and regulatory enforcement are changing how open Apple and Google must be to external payment options across major markets. The United States, the European Union, Japan, and South Korea are all moving, but not at the same pace or in the same direction.

The opportunity is real. For merchants selling subscriptions, digital content, virtual items, memberships, and other digital goods or services, external purchase paths may help reduce the platform service fees associated with traditional in-app purchase models.

Merchants gain more operating control. External purchase paths can give merchants more flexibility over payment methods, user experience, pricing incentives, and customer operations.

There is no single global playbook. Rules differ by market across entry points, in-app purchase or platform billing requirements, reporting obligations, attribution windows, and tax responsibilities.

The practical starting point is a controlled pilot. Merchants should usually begin with high-value, high-frequency, trusted, and established user scenarios before deciding whether to expand.

Platform payment rules may look like a legal or policy issue, but they directly affect revenue models and user operations. The possibility of lowering costs compared with traditional in-app purchase rates that can reach 30% is meaningful. Yet whether that turns into real margin depends on what remains after payment processing costs, tax, risk management, customer support, and conversion loss.

External purchase paths can also give merchants more room to shape the checkout experience: offering more local payment methods, designing incentives for high-value users, and customizing the purchase journey in ways that are difficult under a fully platform-controlled billing model.

That is why external purchase and billing options should not be evaluated only through the question of “how much can we save?” They are closer to a rebuild of the monetization flow. On the front end, merchants need to understand whether users are willing to take an additional step. On the back end, they need to handle payment acceptance, reconciliation, refunds, fraud, and tax. Before calculating the upside, the first task is to understand how rules differ by path and by market.

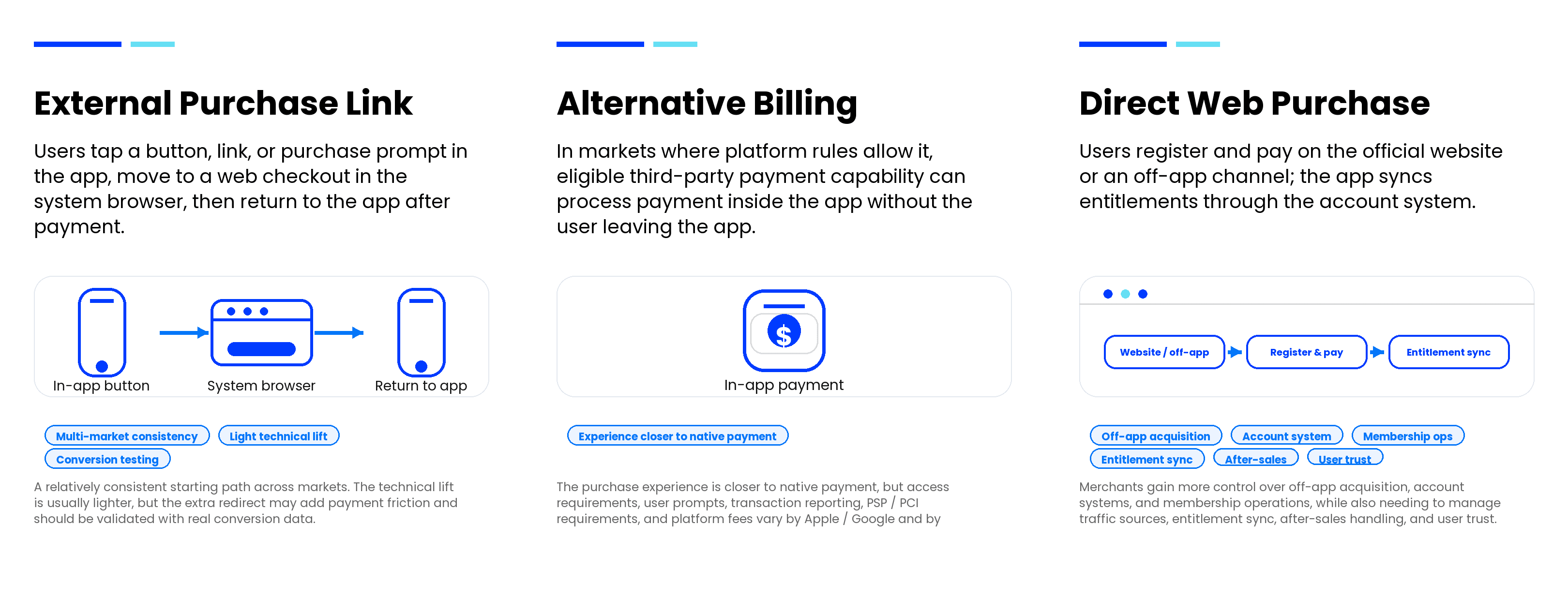

Three paths with different trade-offs

In markets where external purchase options are allowed, there is more than one way to implement them. Where the entry point appears, who processes the transaction, and whether the user leaves the app all affect review risk, conversion performance, and downstream operating costs.

The three most common paths are:

Start with the market, then evaluate the rules

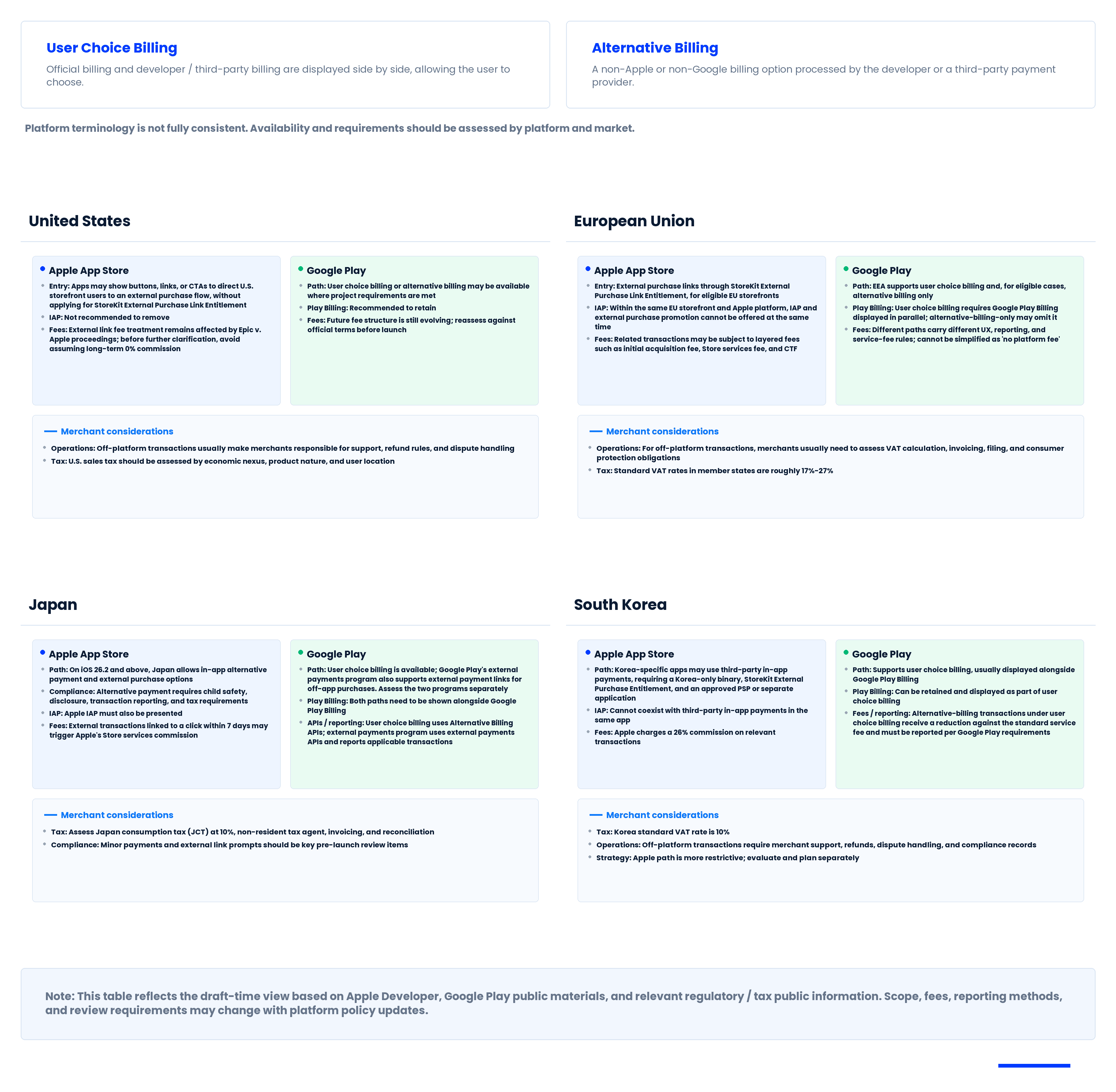

The complexity of external purchase and billing options comes from market differences. The United States, the European Union, Japan, and South Korea vary significantly in openness, entry-point design, platform billing requirements, reporting obligations, attribution rules, and tax responsibilities.

Before engineering teams start planning implementation details, merchants need a market-by-market view of what is currently possible.

Overall, the United States remains one of the clearest markets for early validation of external purchase flows:

Merchants can design an external purchase experience and, in eligible app scenarios, guide U.S. users to complete purchases on the web through buttons, links, or purchase prompts.

Where platform rules allow it, merchants can show web pricing benefits, offer cards, PayPal, and other familiar payment methods, and design differentiated incentives for higher-value users.

Merchants can use this window to test conversion, payment completion, and net revenue retention while building transaction records, tax processes, and operating workflows before long-term fee structures become more settled.

The European Union and Japan are more granular. Japan, for example, is opening not only payment paths but also parts of app distribution, including alternative app marketplaces. The value of preparing for these markets is therefore not only near-term fee reduction. It is also about building the infrastructure for entitlements, reporting, child-safety requirements, tax, and customer support.

From day one, merchants should design external purchase flows against the strictest market they expect to support. That means using the appropriate system browser, StoreKit APIs, platform-specified flows, transaction records, and reporting capabilities where required. Designing this way reduces the risk of rebuilding the flow later.

South Korea should be evaluated separately, especially for merchants operating across both iOS and Android. It should not be folded into a single global rollout plan without a dedicated market assessment.

Should merchants move now?

The value of external purchase and billing options is real, but the decision is ultimately about revenue structure: how much of the platform service fee reduction can be retained after new operating costs are added? The answer depends on the merchant’s business scale, user loyalty, and market footprint.

In practice, four types of businesses are more likely to benefit from early evaluation.

1. The core business is digital goods or services

This includes subscriptions, virtual goods, paid content, memberships, and digital services. Physical goods are outside the mandatory IAP scope and are not the focus of this article.

2. The merchant has a business base or long-term plan in the target market

External purchase and billing options are not a paper exercise. They only matter if they affect real orders and operating outcomes. If a merchant is still at an early stage in a target market, with limited revenue contribution, investing too early in checkout redesign, support operations, risk controls, and tax workflows may not be justified.

The strongest candidates usually have:

an established user base;

recurring or sustained revenue;

clear market-level operating goals.

3. Order value and user loyalty can absorb checkout friction

External purchase flows often add steps to the payment journey. If order value is low, brand trust is weak, or purchase intent is highly impulsive, the benefit of lower payment-related costs may be offset by conversion loss.

Merchants should prioritize evaluation when they have:

higher average order value;

stronger brand trust or user loyalty;

clear purchase intent;

frequent repeat purchases, such as subscriptions or in-game virtual assets.

4. The merchant can take on the operating responsibility

When a transaction moves from in-app billing to the web or another external purchase path, risk management, disputes, after-sales support, tax calculation, and filing responsibilities shift closer to the merchant. Moving too quickly without preparation can create more complexity than value.

The better starting point is a high-value, high-frequency, trusted scenario where the merchant can control the cost of testing while quickly validating the real business impact.

More than adding a button

External purchase flows are often described as “adding a checkout button.” In practice, they require a stable, compliant, and sustainable end-to-end operating flow.

Payment flow stability is a prerequisite

External purchase flows involve multiple technical and user-experience steps. Any friction in the process can lead to interrupted orders, payment failures, and user drop-off.

Merchants should evaluate local payment preferences, payment method coverage, redirect experience, and checkout stability before launch. After launch, they should monitor payment completion rate, failure reasons, and abnormal fluctuations.

Risk and support become more direct responsibilities

Taking over the transaction gives merchants more flexibility, but fraud, stolen-card activity, refunds, and user disputes also become more visible in business results.

Risk controls should be built into the full transaction lifecycle. Merchants also need clear refund, support, and dispute-handling mechanisms to protect user trust and transaction quality.

Tax compliance is easy to underestimate

When transactions move to external purchase links or alternative billing, merchants may become the seller of record in more situations. They need to assess sales tax, VAT, JCT, and other calculation, filing, and after-sales responsibilities.

Merchants should clarify tax calculation and filing requirements early, and bring in payment, tax, and compliance expertise at the right stage.

They also need sustainable internal processes for market-specific rules, operational execution, and record retention.

Assess the opportunity, then choose the path

External purchase and billing options are creating new opportunities for app businesses, but they are not a universal answer for every merchant. Several questions need to be answered before launch:

Which path best balances implementation cost, payment experience, and rule requirements?

After accounting for redirect friction, tax, risk, and operating costs, how much of the fee reduction can actually be retained?

Part 2 of this series looks at the operating economics in more detail: what merchants may save, which costs are often underestimated, and how to design a controlled pilot.

If you are evaluating whether external purchase and billing options fit your business, PayerMax can help you assess target markets, product scenarios, user paths, and operating requirements.